Why Do We Use N-1 in Sample Variance? The Hidden Truth Behind Accurate Experimentation

Posted on September 25, 2025

Have you ever wondered why statisticians always subtract 1 instead of dividing by N when calculating sample variance? At first glance, it feels like a small adjustment, but this mysterious “N-1 rule” is the reason experiments, whether in science or A/B testing, yield reliable insights. Without it, your results can become misleading, potentially costing businesses thousands in wrong decisions. So, what’s the secret behind this subtraction, and why does it matter so much for marketers, product managers, and growth teams running experiments today?

Why Does the N-1 Matter in Sample Variance?

When calculating variance, we’re essentially measuring how much individual data points deviate from the mean. If we had access to the entire population, we’d divide by N. But in the real world—whether it’s medical trials or A/B testing button colors—we rarely have the entire population. We work with samples, small slices of the bigger picture.

Here’s where the catch lies:

Using N directly in samples tends to underestimate the true variance.

This underestimation makes results appear more confident than they really are.

By subtracting 1, we apply what’s known as Bessel’s Correction. This correction accounts for the fact that we’re estimating from limited data, giving a more accurate reflection of uncertainty.

A Real-World Analogy

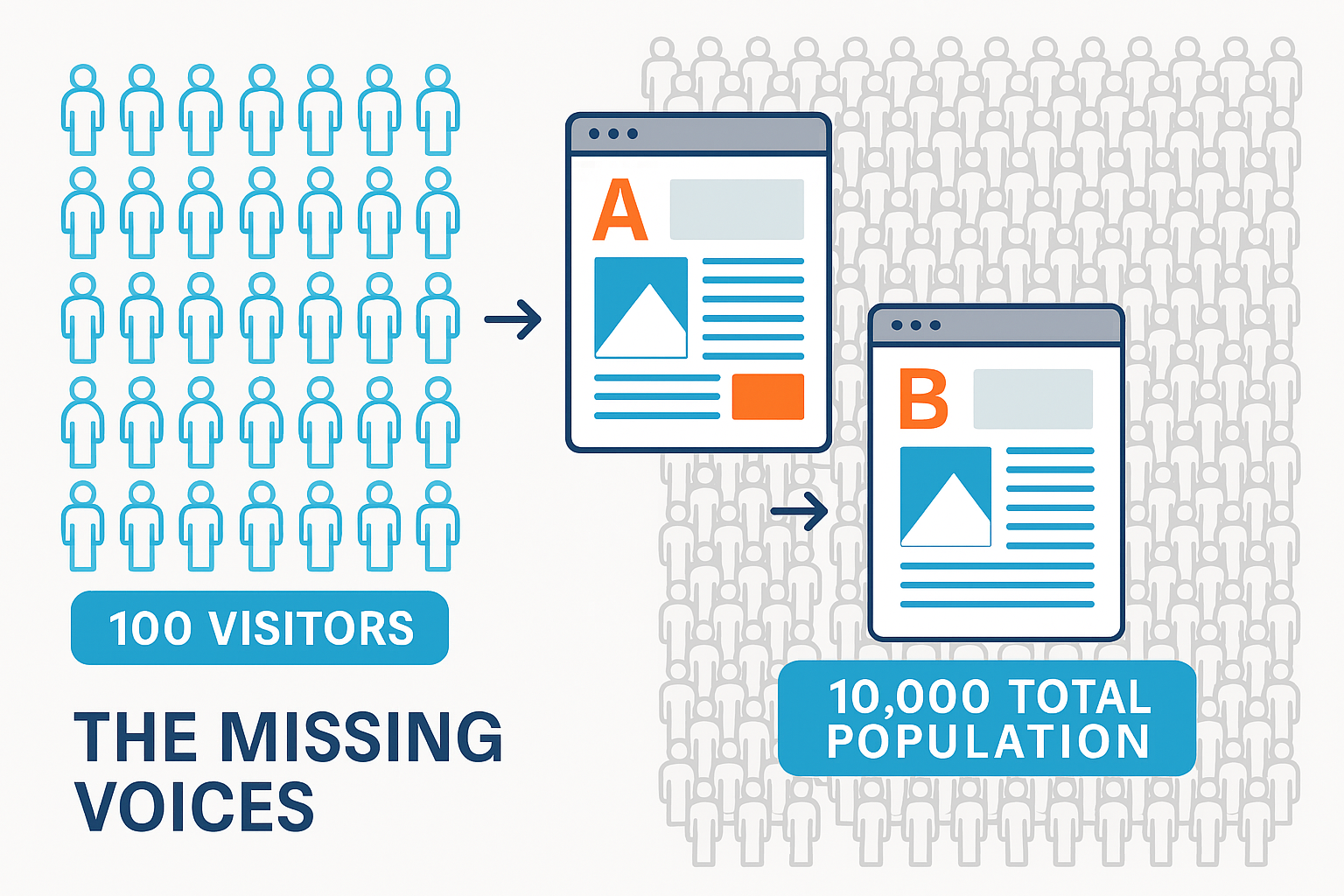

Imagine you’re testing two different landing page headlines. You only gather responses from 100 visitors, not your entire customer base of 10,000. If you simply divided by 100 (N), you’d bias your results toward being overly certain. The correction (N-1) ensures your variance accounts for the missing voices in your dataset—protecting you from making a bad marketing decision based on false confidence.

The Mathematics in Simple Terms

The formula for sample variance is:

s2=∑(xi−xˉ)2n−1s^2 = \frac{\sum (x_i - \bar{x})^2}{n-1}

Where:

xix_i = each data point

xˉ\bar{x} = sample mean

nn = sample size

By dividing by n-1 instead of n, we’re correcting the bias and ensuring our sample variance is an unbiased estimator of the population variance.

Why This Matters for A/B Testing

Direct Experiment, like any modern A/B testing tool, relies on statistical rigor to ensure that experiment results aren’t misleading. Imagine rolling out a new product feature because your test said it “performed better,” only to find it flops when exposed to the entire customer base.

Using N-1 in variance calculations is what keeps experiment results aligned with the real-world impact. It:

Prevents overconfidence in small sample results.

Ensures confidence intervals reflect actual uncertainty.

Helps teams avoid false positives when declaring a “winning” variation.

In short, N-1 makes your A/B tests trustworthy and actionable.

The Hidden Cost of Ignoring the N-1 Rule

Let’s say you ignore this correction and divide by N. Your test might report that variation B outperforms variation A with 95% confidence. Exciting, right?

But because variance was underestimated, your confidence is inflated. When you scale that change across millions of users, the performance may collapse. Suddenly, what looked like a win in testing becomes a business setback.

This is why Direct Experiment integrates the proper statistical methods—including N-1 corrections—so that every result you see has been adjusted for real-world reliability.

FAQs

Q1. Why do we subtract 1 in sample variance but not in population variance?

For a population, we have complete data, so no correction is needed. In a sample, the mean is itself an estimate, which introduces bias. Subtracting 1 corrects that bias.

Q2. Does N-1 always apply in statistics?

No, it specifically applies when estimating variance or standard deviation from samples. Other metrics may not need the correction.

Q3. How does this impact A/B testing tools like Direct Experiment?

Accurate variance ensures correct p-values and confidence intervals. Without N-1, tests would produce unreliable winners, leading to flawed product or marketing decisions.

Q4. What happens if I have a very large sample size?

As N grows very large, the difference between dividing by N and N-1 becomes negligible. But for most business experiments with smaller samples, it matters a lot.

Q5. Is this the same as Bessel’s Correction?

Yes, subtracting 1 is known as Bessel’s Correction, named after the mathematician Friedrich Bessel.

Final Takeaway

The small adjustment of subtracting 1 in sample variance calculations is not just a statistical quirk—it’s a safeguard for truth. For businesses running experiments, it ensures that decisions are based on real-world probabilities, not illusions of certainty.

Direct Experiment builds this statistical rigor into its platform, so every test result you see is trustworthy, actionable, and free from the hidden bias of underestimating variance.